Coarse-Fine Volatility¶

Description¶

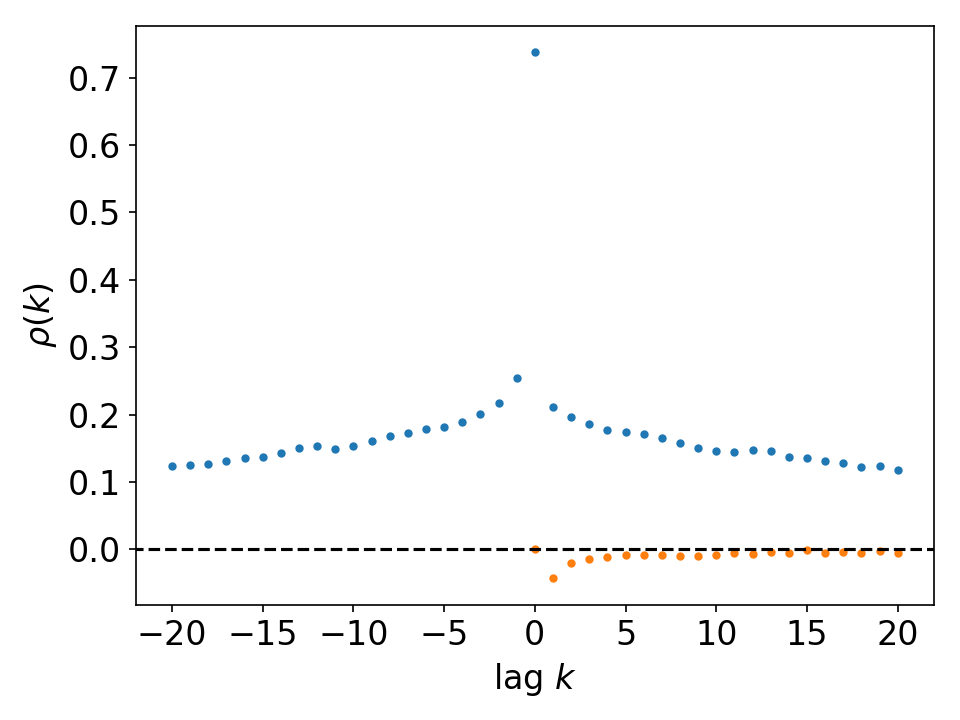

The coarse-fine volatility correlation is a multi-time-scale analysis of volatility.

\begin{eqnarray}

v_{c}^{\tau}(t)&=&\bigg{|}\sum_{i=1}^{\tau}{r_{t-i}}\bigg{|}\\

v_{f}^{\tau}(t)&=&\sum_{i=1}^{\tau}{|r_{t-i}|}.

\end{eqnarray}

While the coarse volatility is the absolute value of the price movement in \(\tau\) days, the fine volatility is the sum of the absolute price return in \(\tau\) days. \(\tau=5\) is starndard as it stands for day-week time-scales.

\begin{equation}

\rho_{cf}^{\tau}(k)=Corr(v_{c}^{\tau}(t+k),v_{f}^{\tau}(t)).

\end{equation}

[Muller_1997][Gavrishchaka_2003] reported that there exists the negative asymmetry of the lead-lag correlation quantified by the difference

\begin{equation}

\Delta\rho_{cf}^{\tau}(k)=\rho_{cf}^{\tau}(k)-\rho_{cf}^{\tau}(-k).

\end{equation}

Fig. Averaged result for S&P500 firms daily price return

Code Example¶

import datetime as dt

import pandas_datareader.data as web

import numpy as np

import stylefact.finance as sff

import stylefact.visualize as sfv

st = dt.datetime(1990,1,1)

en = dt.datetime(2020,1,1)

data = web.get_data_yahoo('GM', start=st, end=en)

prices = data['Adj Close'].to_numpy()

log_prices = np.log(prices)

returns = np.diff(log_prices)

x,y = sff.coarsefine_volatility(returns)

sfv.coarsefine_volatility(x,y,'coarsefine')

References¶

| [GG03] | V. V. Gavrishchaka and S. B. Ganguli. Volatility forecasting from multiscale and high-dimensional market data. Neurocomputing, 55(1):285–305, 2003. |

| [MDD+97] | Ulrich A. Müller, Michel M. Dacorogna, Rakhal D. Davé, Richard B. Olsen, Olivier V. Pictet, and Jacob E. von Weizsäcker. Volatilities of different time resolutions - analyzing the dynamics of market components. Journal of Empirical Finance, 4(2):213–239, 1997. |