Gain/Loss Asymmetry¶

Description¶

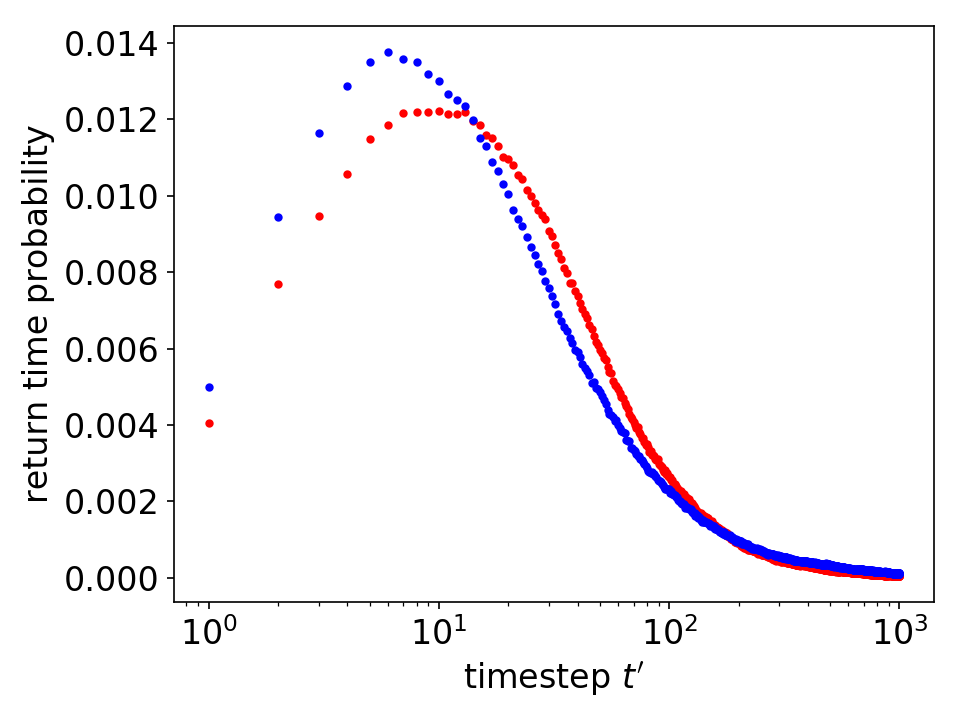

The gain/loss asymmetry refers to the observation that the speed of price fall is faster than that of the price rise. [Jensen_2006]

\begin{equation}

T^{t}(\theta) = \left\{ \begin{array}{ll}

\inf{\{ t'| \log{p_{t+t'}}-\log{p_{t}} >=\theta,t'>0 \}} & (\theta>0) \\

\inf{\{ t'| \log{p_{t+t'}}-\log{p_{t}} <=\theta,t'>0 \}} & (\theta<0).

\end{array} \right.

\end{equation}

Fig. Averaged result for S&P500 firms daily price return

Code Example¶

import datetime as dt

import pandas_datareader.data as web

import numpy as np

import stylefact.finance as sff

import stylefact.visualize as sfv

st = dt.datetime(1990,1,1)

en = dt.datetime(2020,1,1)

data = web.get_data_yahoo('GM', start=st, end=en)

prices = data['Adj Close'].to_numpy()

log_prices = np.log(prices)

returns = np.diff(log_prices)

positive_dist,negative_dist = sff.gainloss_asymmetry(returns)

sfv.gainloss_asymmetry(positive_dist,negative_dist,'gainloss_asymmetry')

References¶

| [Bac00] | Louis Bachelier. Théorie de la spéculation. Annales Scientifiques de l’École Normale Supérieure, 3:21–86, 1900. |

| [CTPA11] | Anirban Chakraborti, Ioane Toke, Marco Patriarca, and Frédéric Abergel. Econophysics review: i. empirical facts. Quantitative Finance, 11(7):991–1012, 2011. |

| [Con01] | Rama Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223–236, 2001. |

| [GG03] | V. V. Gavrishchaka and S. B. Ganguli. Volatility forecasting from multiscale and high-dimensional market data. Neurocomputing, 55(1):285–305, 2003. |

| [JJS06] | Mogens H. Jensen, Anders Johansen, and Ingve Simonsen. Inverse statistics in economics: the gain-loss asymmetry. Physica A, 324(1-2):338–343, 2006. |

| [MDD+97] | Ulrich A. Müller, Michel M. Dacorogna, Rakhal D. Davé, Richard B. Olsen, Olivier V. Pictet, and Jacob E. von Weizsäcker. Volatilities of different time resolutions - analyzing the dynamics of market components. Journal of Empirical Finance, 4(2):213–239, 1997. |